GUIDE TO QUANTITATIVE RISK ANALYSIS

TCM Framework: 7.6 - Risk Management

Rev. March 18, 2024

|

AACE® International Professional Guidance Document No. 02 GUIDE TO QUANTITATIVE RISK ANALYSIS TCM Framework: 7.6 - Risk Management Rev. March 18, 2024 |

|

This document is copyrighted by AACE International and may not be reproduced without permission.

QRA Principles and Method Types – RP 40R-08

QRA Principles and Method Types – Escalation and Currency

Hybrid or Combined Methods and Aggregation of Projects

Complexity, Systems, Behavior, and QRA

Key Terminology – RP 10S-90

Guide to Specific Method RPs (In PGD Map Numerical Order)

1. Understanding the Project System (Stage-Gate Process) and Scope

2. Understanding Estimate Classification (Level of Scope Definition)

3. Value Management: Capitalize on Opportunities

4. Understanding the Base Estimate and Schedules: Basis Documents and Reviews

5. Understanding Concepts and Principles of QRA

6. Quantify the Bias Using Validation/Benchmarking

7. Quantify Uncertainty and Risk in Support of Decision MakingPredetermined Guidelines

Parametric Method

Simulation (Monte-Carlo Simulation)

Hybrid Methods

EscalationLong-Range/Life Cycle (Class 10)

Complexity/Non-Linearity Methods

Programs and Portfolios

Management Reserves8. Application of QRA in Strategic Asset (Portfolio) Management

9. Project Control Planning and Contingency Allocation

10. Change Management and Contingency Management

11. Maintain Methods and Tools Considering Historical Data

Methods

Application Guide

References

Contributors

Professional guidance documents (PGDs) provide roadmaps to improve use and understanding for collections of related AACE International® (AACE) recommended practices (RPs). They provide clarification on their purpose, function, context, and inter-relationships so that users can locate and focus on those RPs that best meet their requirements. The PGDs also highlight in-progress and preliminarily planned RPs to inform and guide AACE RP development (contact the Decision and Risk Management (DRM) Technical Subcommittee if interested in RP development). A hyper-linked format is used instead of publishing a standard text (which would have hundreds of pages of content). In recognition of the fact that AACE RPs are living documents, always refer to the latest RP. RPs are available free to AACE members (JOIN AACE).

PGDs also support the Total Cost Management (TCM) Framework in which RPs relating to each chapter are listed but not described. The heart of most PGDs is a map showing the relationship of the RPs in the context of the subject TCM process (and other TCM processes). This PGD covers RPs for the quantitative risk analysis (QRA) steps in the TCM Chapter 7.6 Risk Management process map (re: TCM Figure 7.6-1) and also support the Chapter 3.2 Asset Planning process map (re: TCM Figure 3.2-1). Key uses of QRA in TCM are to support contingency and other risk funding determinations for projects and programs, to support investment alternative evaluation and selection and to support capital portfolio management. This covers both the project, and the asset life cycles. This PGD was developed because of strong interest in the QRA area of practice, particularly in contingency. Many have an established project risk management process but lack reliable risk quantification. Also, there is a robust set of RPs to choose from in this area, justifying PGD treatment.

While there are no RPs for analytics methods at this time (e.g., machine learning and artificial intelligence), there are commercial applilcations on the market. Therefore, this RP touches on the topic including paper reference(s). At this time, in respect to data-driven methods, RP 114R-20, Project Historical Database Development, sets the stage for analytics application, and RP 42R-08, Risk Analysis and Contingency Determination Using Parametric Estimating, with its use of multiple linear regression (MLR) provides an entry point for analytics. Also, the RP 122R-22, Quantitative Risk Analysis Maturity Model, establishes the use of analytics as a QRA stretch goal (i.e., level 5).

QRA covers a broad set of practices used primarily to quantify uncertainty and risks in a way that supports asset planning and investment decision analysis (TCM 3.2 and TCM 3.3), change management decisions (TCM 10.3), and cost and schedule contingency, reserves, escalation and other phased project funding and control basis determinations (TCM 8.1). However, the focus of this PGD is TCM 7.6 which summarizes the QRA step as: “For each risk selected by the team for quantitative risk analysis, a probabilistic estimate of its impact will be prepared. The chosen methodology will have been specified during the risk planning phase.”.

This PGD also covers fundamental QRA RPs such as for selecting probability density functions as well as highlighting key QRA terms as defined in AACE RP 10S-90, Cost Engineering Terminology. QRA practices intersect with (and may be part of) base cost estimating and scheduling practices upstream of the QRA (e.g., historical data analysis and estimate and schedule validation to quantify bias) as well as control of the risk funds and contingency durations downstream of the QRA (e.g., contingency drawdown assessment). These related RPs will be highlighted where applicable.

It should be noted that PGD-01, Guide to Cost Estimate Classification Systems, addresses the concept of accuracy; a shorthand expression of the uncertainty characteristic of estimates. The classification RPs recommend that accuracy be determined through the application of appropriate QRA methods (i.e., there are no standard accuracy ranges). This guide addresses the appropriateness of the various QRA methods for different project phases and types. Given that accuracy is a key concept and communication challenge, RP 104R-19, Communicating Expected Estimate Accuracy (see video) may be considered the start of the map and journey into QRA. Next, RP 40R-08, Contingency Estimating – General Principles, covers the principles of recommended contingency and related methods. From there, the QRA RPs cover the alternative methods in detail, and this PGD’s map shows the path to related RPs and the relationship to other TCM processes.

Given that a purpose of this PGD is to guide users to RPs that best meet their requirements, the RP descriptions in this document include comparative information. For example, the appropriate method may vary depending on the size of the project, the level of scope development, or the resources available to the organization. No single method addresses all situations. Each RP should address the method’s strengths and weaknesses; this PGD brings some of this information to a single reference. In the end, users must study the RPs themselves to make the best method selection. A key RP to review in respect to assessing QRA requirements is RP 122R-22, Quantitative Risk Analysis Maturity Model.

Where RPs are needed to address the TCM 7.6 or other processes, but not yet developed, they are identified. The intention is to update the PGD regularly as RPs and DRM Subcommittee plans are updated. Where RPs are proposed or in process, key references (primarily AACE Transaction papers and books by RP contributors) are noted with links provided in lieu of the pending RP.

The AACE

Decision and Risk Management

Technical Subcommittee began planning an RP

series in 2007 with the initiation of a project to develop the Decision and Risk

Management Professional (DRMP) certification. An early challenge the team of

subject matter experts (SMEs) faced was which of the existing QRA methods to

recommend. QRA is an evolving field of practice and not settled science. The

approach selected was to first establish the principles that any recommended

practice should follow (re:

RP 40R-08). Then each candidate method was compared

to how well it met the principles. Only a limited set of methods met the

criteria.

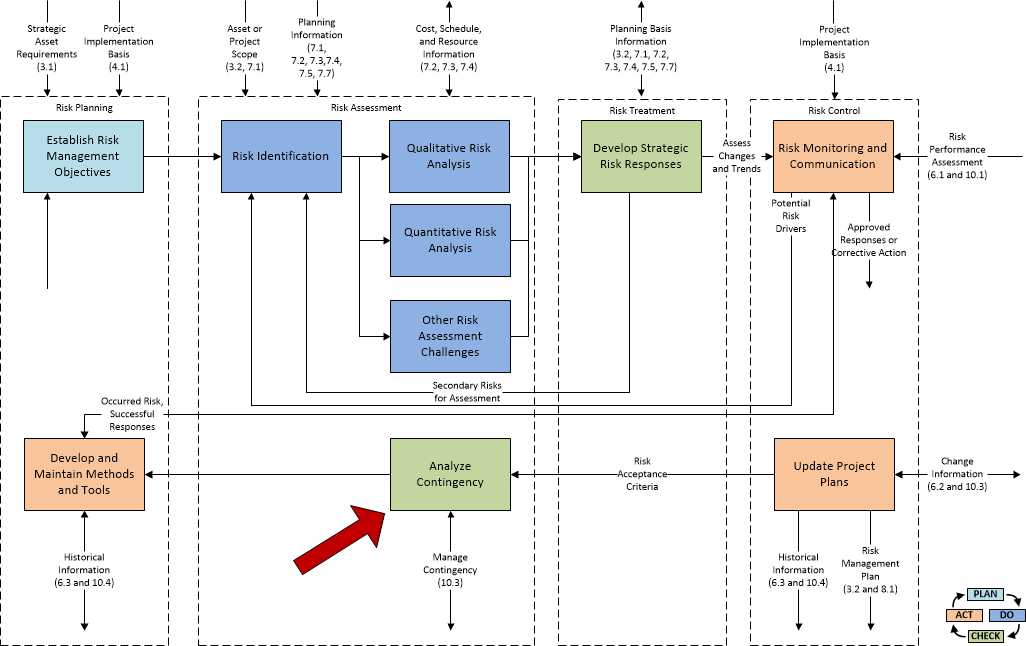

In all cases, the RPs are aligned with the TCM Framework process for risk management (TCM 7.6) and other TCM processes to which TCM 7.6 is linked (TCM 3.2 perhaps being most significant). TCM 7.6 is the only industry risk management process that includes explicit steps for QRA. The TCM risk management process map in Figure 1 depicts that when a phase-gate decision is to be made, the RM process loops back through risk assessment for QRA (the step labeled “Analyze Contingency”). The term contingency in the map is shorthand for any quantified cost or time allowance for risks. This would include quantification for minor decisions over the project life-cycle (such as those made as part of the change management process (per TCM 10.3)) or for major over-arching analyses and decisions over the asset life cycle (such as those made as part of asset planning (per TCM 3.2)).

Figure 1. Process Map for Risk Management (Figure 7.6-1 from the TCM Framework; 2015 edition)

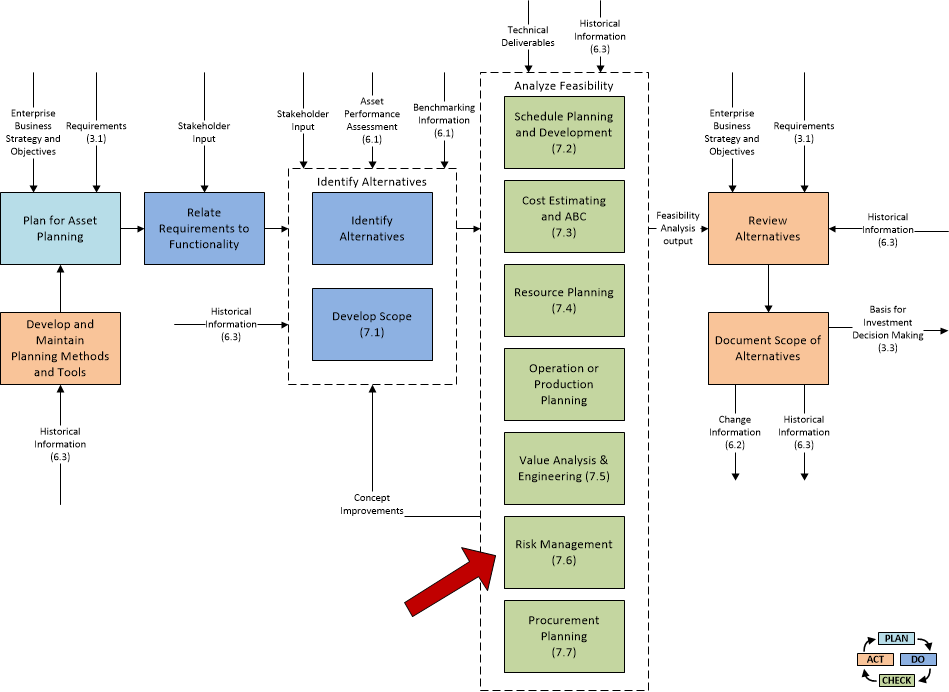

The TCM asset planning process map in Figure 2 (TCM 3.2) depicts the use of risk management, including QRA, in asset alternative analysis which usually involves asset life cycle and portfolio management considerations. This is where unclassified/Class 10 estimates (re: PGD-01) with long-range time horizons and special QRA considerations come into play.

Figure 2. Process Map for Asset Planning (Figure 3.2-1 from the TCM Framework; 2015 edition

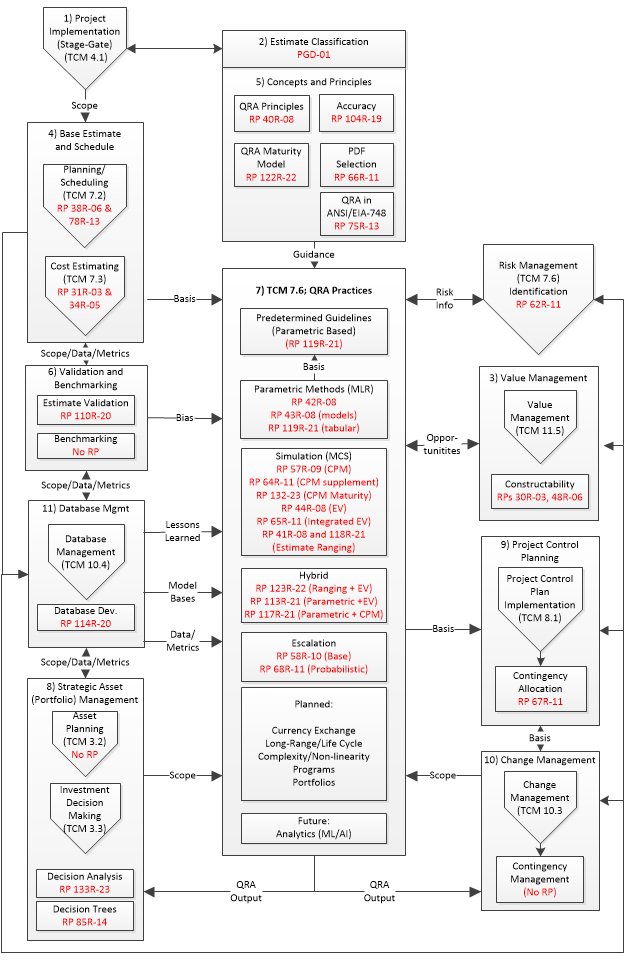

The index map in Figure 3 presents the above processes in a way that highlights the relationship of the many existing and proposed QRA RPs (in red font) in the context of the related TCM Framework processes. The Figure 3 map highlights general information flow linkages between QRA fundamentals and practices and the associated TCM processes or process groups starting with Risk Management (TCM 7.6) (note: QRA practice is not limited to these processes) and including:

Asset Planning and Investment Decision Making) (TCM 3.2 and TCM 3.3);

Project Implementation, Scheduling and Estimating (including Validation and Benchmarking) (TCM 4.1, TCM 7.2 and TCM 7.3);

Project Control Plan Implementation and Change Management) (TCM 8.1 and TCM 10.3);

Database Management (TCM 10.4).

Figure 3. QRA Index Map: QRA RPs in the TCM Framework Context

The following list summarizes the key TCM processes and their respective QRA RPs as shown in the Figure 3 QRA index map. They are listed in a suggested order of study for a practitioner new to QRA. The later “Guide to Specific Method RPs” section of this PGD is organized in this same order.

Understanding the Project System (Stage-Gate Process) and Scope (TCM 4.1) (No RPs)

Understanding Estimate Classification (Level of Scope Definition) (TCM 7.3) (PGD No. 01)

Understanding Value Management (Opportunities) (TCM 11.5) (RP 30R-03 and RP 48R-06)

Understanding the Base Estimate and Schedules (TCM 7.3 and 7.2) (RP 31R-03, RP 78R-13, RP 34R-05, RP 38R-06)

Understanding Concepts and Principles of QRA (TCM 7.6) (RP 40R-08, RP 66R-11, RP 104R-19, RP 122R-22, and RP 132R-23)

Quantify the Bias using Validation & Benchmarking (TCM 6.1, TCM 7.2, and TCM 7.3) (RP 110R-20 and -TBD-)

Quantify Uncertainty and Risk in Support of Decision Making (TCM 7.6) (See Guide to Specific Method RPs later)

Application of QRA in Strategic Asset (Portfolio) Management (TCM 3.2 and TCM 3.3) (RP 85R-14 and RP 133R-23)

Project Control Planning and Contingency Allocation (TCM 8.1) (RP 67R-11)

Change Management and Contingency Management (TCM 10.3) (No QRA-focused RPs)

Maintain Methods and Tools considering Historical Data (TCM 10.4) (RP 114R-20)

Prior to the “Guide to Specific Method RPs” section, the next sections address some QRA-related fundamentals including:

QRA PRINCIPLES AND METHOD TYPES – RP 40R-08

RP 40R-08, Contingency Estimating – General Principles provides a summary and description of the general QRA principles. In summary, the principles are:

Meet client objectives, expectations and requirements

Part of and facilitates an effective decision or risk management process (e.g., TCM)

Fit-for-use

Starts with identifying the risk drivers with input from all appropriate parties

Methods clearly link risk drivers and cost/schedule outcomes

Avoids iatrogenic (self-inflicted) risks

Employs empiricism

Employs experience/competency

Provides probabilistic estimating results in a way the supports effective decision making and risk management

RP 40R-08 describes in detail what is considered with each principle. These principles are fundamental considerations in the QRA Maturity Model described in a later section (RP 122R-22). The principles are not all repeated here, but as an example of the principle perhaps most applicable to the purpose of this PGD, consider the fit-for-use principle description:

Fit-For-Use

In addition to considering the general requirements of the client and the process, the practitioner must also consider any other significant contextual characteristics that may or may not affect the estimating practices selected and how they are managed and/or performed. These include, but are not limited to the following:

Portfolio, Program or Project Type: Scope, size, complexity, level of technology

Risk Type: Strategic versus tactical, systemic versus project-specific

Project Phase: Estimate/schedule class

Base Estimate/Schedule Methodologies: Methods, tools, and data used to develop the estimate or schedule (without risk cost/time included)

Skills and Knowledge: Of both the practitioner and other participants

As should be evident, no single QRA method can be best in addressing all

these characteristics. This PGD focuses on the above fit-for-use

characteristics for each method, while also highlighting how an RP addresses

other principles as appropriate (see the "Methods Application Guide" section).

RP 40R-08 also provides a general categorization of common QRA method types, and also has a table of how each general type addresses the principles. This is a starting point for method selection. However, this PGD adds to it with the "Methods Application Guide". The RP 40R-08 general QRA method types are as follows (analytics will be a future addition):

Expert Judgement

Predetermined Guidelines (with varying degrees of judgment and empiricism used)

Simulation Analysis (primarily expert judgment incorporated in a Monte Carlo simulation (MCS))

Parametric Modeling (empirically-based algorithm, usually derived through multiple linear regression (MLR) analysis (will transition to machine learning/AI), with varying degrees of judgment used)

Hybrid (some combination of the above)

QRA PRINCIPLES AND METHOD TYPES – ESCALATION AND CURRENCY – RP 68R-11

RP 68R-11, Escalation Estimating Using Indices and Monte Carlo Simulation adds further QRA principles specific to escalation and currency analysis as follows:

Expert Judgement

Differentiate between escalation, currency and contingency

Leverage economist’s knowledge (based on macroeconomics)

Use indices appropriate to each account including addressing differential price trends between accounts

Use indices that address levels of detail for various estimate classes

Leverage procurement/contracting specialist’s knowledge of markets

Ensure that indices address the specific internal and external market situation

Facilitate estimation of appropriate spending or cash flow profile

Calibrate or validate data with historical data

Use probabilistic methods

Use the same economic scenarios for both business and capital planning

Apply in a consistent approach using a tool that facilitates best practice

Integrate in a total cost management (TCM) process

RP 68R-11 calls for the use of probabilistic methods for escalation. Applying a probabilistic method should be considered for all projects of long duration (e.g., mid-point of spending >18 months from the starting date) because escalation may be the most uncertain cost element on a project and it has significant impacts to net present value (NPV). The following communication points will help explain to business and finance stakeholders why a probabilistic method may be appropriate:

Escalation is not negated by the discount rate used in net present value (NPV) methods.

Escalation includes inflation but it is not the same; it tends to be more volatile and varied by cost type.

CAPEX escalation trends are not balanced by sell price (revenue) trends; i.e., their risks do not cancel out in NPV analysis. For example, CAPEX prices are sticky; when product sell prices decline after a boom, capex prices may not (re: probabilistic escalation supports the alignment of business and capital planning).

Currency or exchange rate risk is somewhat related to escalation as both are driven by economic conditions. AACE does not yet have a currency QRA RP. However, the principles and methods used for probabilistic escalation are essentially the same as for currency. Currency adds to the equation the need to forecast future spending not only by cost account, but by currency. Exchange rate indices are then used to assess the uncertainty resulting from varying valuation of currencies as-expended relative to the base estimate currency. Where it is a major risk, finance departments may indemnify the project for currency risk (e.g., via hedging) making it less of a project team issue.

It should be noted that escalation is particularly sensitive to project

schedule risk; i.e., schedule slip pushes spending into later time periods with

potentially significant escalation cost impact. Also, escalation is applied to

contingency (which has the same date basis as the rest of the base cost

estimate). Because both cost growth and schedule slip are quantified as part of

contingency QRA, it should be obvious that contingency and escalation

quantification are optimally integrated with escalation analysis following QRA

for contingency.

QRA MATURITY MODEL (QRAMM) – RP 122r-22

RP 122R-22, Quantitative Risk Analysis Maturity Model defines a method for assessing the level of capability for quantifying the uncertainty and risks associated with projects, programs and portfolios within the risk management function of a capital investment or project management organization. The QRAMM is not prescriptive to specific QRA methods; it highlights that many options exist (as covered here in PGD-02 and aligned with the principles in RP 40R-08) and provides examples of how various methods may be considered at various maturity levels as appropriate.

The QRAMM is also not a maturity model for assessing the depth of capability for

any particular QRA method selected by an organization (e.g., see paper on a

model for CPM-based QRA [1]). Instead, the QRAMM offers a point of reference or

road map to facilitate continuous improvement. Each QRAMM capability level (it

defines five levels of maturity) can be applied with various degrees of rigor or

maturity depending on the organization needs. The QRAMM assumes that to achieve

a high level of QRA maturity, an organization must clearly understand it’s risk

management needs and apply any particular QRA method to the degree that is

fit-for-purpose for those needs. A basis of the QRAMM is that the highest level

(i.e., Level 5) be set as an aspirational or stretch goal, with the current

aspiration being to apply analytics in QRA.

QRA INPUTS: DATA, ELICITATION, AND BIAS – RP 62R-11

QRA methods require various information inputs about uncertainties and risks (review the section on "QRA Risk Taxonomy" in the "Key Terminology ̶ RP 10S-90" section first). This includes identified risks and information about their probability of occurrence and potential impacts for project-specific risks. In addition, ratings of systemic risk attributes or parameters are needed for parametric/MLR-based models. Also, ranges of impact are needed for uncertainties (probability = 100%) of all types for non-parametric/MCS methods. The primary sources of information include:

Project Historical Data (RP 114R-20): Asset and project historical data (may be incorporated in a parametric risk model).

Project-Specific Data: Current data on risk drivers including relevant weather history, geotechnical studies, labor and other market studies, and so on.

Subjective Inputs: Information on systemic risk ratings, probabilities for risk events, and impact estimations for non-parametric uncertainties and risks from stakeholders, teams and subject matter experts.

RP 62R-11, Risk Assessment: Identification and Qualitative Analysis addresses methods of eliciting input on the subjective inputs. Elicitation methods such as brainstorming, interviewing, Delphi, structured elicitation, and subject matter calibration are addressed there. One reason these topics are critical to QRA is that subjective inputs are inherently biased; all QRA methods must address bias as one input in order to produce realistic outputs. RP 110R-20, Cost Estimate Validation documents a method to quantify bias in base cost estimates. RP 114R-20, Project Historical Database Development documents capturing project risk information (e.g., past occurred risks and impacts) as well as metrics to assess historical project cost and schedule outcomes as well as bias. See Section 6 on "Quantify the Bias Using Validation/Benchmarking".

In respect to data, analytics (e.g., machine learning and artificial intelligence) represents a key topic; however, there are no QRA RPs on analytics methods at this time. The RP 122R-22, Quantitative Risk Analysis Maturity Model includes the use of analytics as a stretch goal (i.e., Level 5); this applies to the AACE DRM Subcommittee as well.

HYBRID OR COMBINED METHODS AND AGGREGATION OF PROJECTS

An implication of following the QRA principles stated is that there is no

single method that can be used to quantify all risk on a given project.

While a single tool addressing all risk may be possible, such a tool would

sacrifice one or more principles. Therefore, typical combinations of methods are

addressed in the QRA RPs. These include

RP 113R-21 (parametric + expected

value), RP 117R-21 (parametric + CPM) and

RP 123R-22 (estimate ranging +

expected value). Each of these incorporate Monte Carlo simulation at some level.

These two-part combinations address systemic versus project-specific risks (see

"Key Terminology - RP 10S-90" definitions) with the exception of

RP 123R-22

which applies estimate ranging for background variability in lieu of the

parametric method when systemic risks are not significant.

In addition, there are special considerations for and variations of methods when applied in aggregations of projects in a program or portfolio. These topics will also be discussed; however, there are no program or portfolio level QRA RPs at this time.

As stated, QRA is an evolving area of practice, and combination and integration of methods, and application for aggregations of projects, are areas to pay particular attention to developments. Given that it is evolving, QRA is a great area of practice for papers, presentations and for volunteer contributions to RP development.

COMPLEXITY, SYSTEMS, BEHAVIOR, AND QRA

Other areas where QRA is evolving include the understanding and quantification of risk relative to:

Complexity

Systems (the functional nature of capital project, program and portfolio management within the context of external systems)

Behavior (the human nature of capital project, program and portfolio management and decision making)

The trend in industry appears to be towards projects of increasing size or complication (measures of the number of parts) and complexity (measures of the extent and nature of interactions of the parts). There is also greater appreciation of the systems nature of projects for which learnings from systems engineering provide insight. Finally, the impact of human behavior, particularly as evidenced in bias, presents a challenge to quantification.

While there are no specific RPs for these topics at this time (e.g., measuring complexity), some QRA methods address these attributes to some extent and this will be noted where applicable (e.g., parametric methods for systemic risks apply complexity and bias measures). AACE Transaction papers will be highlighted that focus on these issues (e.g., non-linearity of impacts).

KEY TERMINOLOGY – RP 10S-90

The terminology related to QRA is extensive. One QRA text has over 170 terms in its glossary [2]. AACE RP 10S-90, Cost Engineering Terminology is the recommended reference for QRA terminology. The AACE definitions evolved from its 60-plus year history and are believed to reflect “what works best” for its members in general cost engineering and project control application. Other industry definitions often contain what the DRM Subcommittee feels are ambiguities (often originating from a qualitative point of view) on one hand, or over-specificity on the other (to suit specific standards that may or may not apply to one’s situation).

There are a number of terms defining the objects of QRA (the control

accounts or activities being determined), and QRA risk taxonomy worth

highlighting in this PGD because they are fundamental to QRA methods. there are

variations in industry definitions, and they are often misunderstood. These

definitions are:

QRA Objects

Allowances

Contingency

Management Reserves

Escalation

QRA Risk Taxonomy

Systemic Risks vs. Project-Specific Risks

Uncertainties vs. Risk Events

Critical Risks

Always refer to the original source document for the latest definition (in this case RP 10S-90)

|

Allowances |

|

|

|

Discussion:

General uncertainties (e.g., allowance for weather or scope growth allowance) should be quantified in contingency. A rule-of-thumb is that if a cost item cannot be physically progressed, it belongs in contingency.

|

|

Special Case - Design Development

Allowance: |

|

Contingency |

|

|

|

Discussion:

|

|

Special Case - Earned Value

Management Based Upon ANSI EIA 748:

|

|

Special Case - Unclassified/Class10

Estimates:

|

|

Management Reserve |

|

|

|

Discussion:

|

|

Special Case - Earned Value

Management Based Upon ANSI EIA 748:

|

|

Escalation |

|

|

|

Discussion: |

The following risk taxonomy terms define risk types in respect to the most appropriate or fit-for-use method for their QRA. Therefore, understanding their definition is important to selecting and communicating about QRA methods. The following term-pairs (i.e., versus) are discussed with the pairings resulting from QRA method application distinctions:

Systemic versus Project-Specific Risks

Uncertainties versus Risk Events

|

Systemic versus Project-Specific Risks |

|

10S-90 Definitions:

|

|

Discussion:

|

|

Uncertainties versus Risks Events |

|

There is a host of risk taxonomy terms in use for many purposes. For QRA methods that quantify the probability of occurrence (as typically used in probability x impact calculations) an important risk taxonomy distinction is between risks that have 100% probability of occurring and those that have less than 100% probability. The following term usage, which has been proposed for RP 10S-90 (practitioners should monitor the RP for risk terminology development which evolves along with methods), makes this probability distinction:

Uncertainty: A risk with probability of occurrence of 100%; i.e., a risk condition, not a risk event. Other terms found in RP 10S-90 for risks with 100% probability of occurrence are background variability, inherent variability, and inherent risk. Systemic risk, which is an artifact of the project system is also an uncertainty. Project-specific risks, which includes conditions, may be an uncertainty (e.g., 100% probability that site soil conditions or weather will vary from the project plan basis for better or worse).

Risk Event: In respect to risk quantification, an incident or occurrence whose nature or result could be a threat or opportunity to the outcome of the project, and that has a probability of occurrence of < 100%. Contingent risk is sometimes used as a synonym. Project-specific risks are most often risk events (condition uncertainty being an exception). A potential identified change in a project system is a risk event. |

|

Critical Risks |

|

A risk taxonomy designation used to classify project risks for the purposes of selecting a quantification method. A critical risk is an identified condition or event risk that in its own right may materially affect management cost, schedule, profitability or similar quantitative objectives. Specific criteria for rating a risk as critical are established with management concurrence. For quantitative risk analysis, the rating is more specific than qualitative risk analysis rankings (i.e., risk matrix). |

|

Discussion: |

GUIDE TO SPECIFIC METHOD RPS (IN PGD MAP NUMERICAL ORDER)

The following table summarizes the various method RPs available for various QRA purposes. The summary QRA process steps outlined in the Introduction and Figure 1 index map is used to organize this listing as follows. Where there are no RPs yet, AACE Transaction papers or other sources are suggested. The "Methods Application Guide" near the end of the PGD provides comparative information about these methods.

1. Understanding the Project System (Stage-Gate Process) and Scope

|

No RPs |

|

Discussion: |

|

Selected References: [4,5,6,7,8]

|

2. Understanding Estimate Classification (Level of Scope Definition)

|

|

|

Discussion: |

|

Selected References: [9,10,11]

|

3. Value Management: Capitalize on Opportunities

|

|

|

Discussion: |

|

Selected References: [12,13,14]

|

4. Understanding the Base Estimate and Schedules: Basis Documents and Reviews

|

|

|

Discussion:

|

5. Understanding Concepts and Principles of QRA

|

|

|

Discussion:

|

|

Selected References: [15]

|

6. Quantify the Bias using Validation/Benchmarking

|

|

|

Discussion: |

|

7. Quantify Uncertainty and Risk in Support of Decision Making

|

Discussion:

|

|

Discussion: |

|

|

|

Discussion:

The parameters in a model are quantitative ratings of systemic risks (e.g., the estimate classification level number is an example rating of the level of scope definition). The method produces single output distributions for cost and schedule; the challenges this aggregation presents to contingency allocation and management are discussed in those sections. The RP also covers the method to calibrate an existing parametric model (e.g., the RAND model in RP 43R-08) to align with a company’s internal data. RP 43R-08 is an adjunct to RP 42R-08 and includes working Excel® versions of the John Hackney and RAND Corporation parametric models. The Hackney model covers cost, while RAND provided models for both cost and construction schedule. (Note: open the RP using the original Adobe Acrobat Reader to see the links to the Excel attachment). The RAND cost model was used to develop the tables in RP 119R-21.

MLR and the parametric method, being data-driven, might be considered a first step toward machine learning and artificial intelligence (ML/AI) albeit limited to a somewhat static basis in historical data, rather than a dynamic basis in contemporaneous data. It is expected that ML/AI methods will eventually supersede the parametric method. |

|

Hybrid

Use:

|

|

General Discussion:

Note on Joint Confidence:

Note on Hybrid Use: |

|

Plus:

Plus:

|

|

57R-09 Discussion:

|

|

64R-11 Discussion:

This is an adjunct to RP 57R-09; not a stand-alone method. Per the text: This RP discusses key procedural, analytical and interpretive considerations in preparation and application of a CPM model; considerations that were not covered in the broader methodological RPs (i.e., RP 57R-09). Topics include schedule quality, schedule model building, linking risks to activities, and interpreting results. The rigor and complexities of CPM based methods may lead one to use the less imposing EV method (RP 65R-11) for less strategic projects. |

|

132R-23 Discussion: This is a supplement to RP 57R-09 and RP 64R-11. This RP provides a rating scheme from levels 0 to 5 to measure the levels of maturity of an organization’s capability and use of the CPM-based quantitative risk analysis methods covered in RP 57R-09 and RP 64R-11. Note that the levels are not consistent with the quantitative risk analysis maturity model (QRAMM) in RP 122R-22 and the RP does not address the use of CPM-based methods in hybrid application per RP 117R-21. |

|

Hybrid Use: |

|

|

|

44R-08 Discussion: |

|

Hybrid Use: |

|

65R-11 Discussion:

|

|

Hybrid Use: |

|

|

|

41R-08 Discussion:

118R-21 Discussion: |

|

Hybrid

Use: |

|

General Discussion: |

|

Discussion: |

|

Discussion: |

|

This is a hybrid of RP 42R-08 and RP 57R-09 (without the RP 57R-09 use of interviews to quantify systemic risks) for projects of any type that have a quality CPM schedule (typically Class 3 or better). |

|

|

|

Discussion: From the RP text: Defines basic principles and methodological building blocks for estimating escalation using forecasted price or cost indices while also addressing uncertainty using Monte Carlo simulation. RP 58R-10 describes a deterministic or base estimating method while RP 68R-11 is an addendum adding probabilistic and scenario/sensitivity analysis to the base method. The RP starts with extending the RP 40R-08 principles to cover escalation.

A feature of RP 68R-11 is that it uses the distribution outputs from cost and schedule contingency models as inputs to the probabilistic escalation model. This integration produces outcome distributions of not only escalation cost, but total CAPEX including cost and schedule contingency; this universal CAPEX distribution can then be readily applied in probabilistic NPV models. |

|

No RPs |

|

Discussion:

One difference between escalation and currency risk is that finance departments may indemnify the project for currency risk on the premise that through hedging or similar practices, it is their role to somewhat mitigate currency risk, not the project team’s. Also, project cost control may be by currency and risk methods may need to align with control practices. The use of such practices need to be considered for each project. |

|

Selected References: [20,21,22]

|

|

RP -TBD-: QRA for Unclassified/Class 10 Estimates |

|

Discussion:

|

|

Selected References: [3]

Class 10 QRA Method: Hollmann, John, “Risk Analysis and Contingency Estimating for Class 10

Estimates”, AACE International Transactions, RISK-3908, AACE

International, Morgantown, WV, 2022. |

|

No RPs |

|

Discussion: Empirical research has indicated that cost and schedule outcome distributions of actual/estimate metrics are sometimes not well modeled by traditional QRA simulation (e.g., actual distributions sometimes exhibit bimodality, fat/long overrun tails, etc.). It is hypothesized that as complexity and other systemic risks increase, the failure mode of projects can shift from orderly to disorderly or chaotic (e.g., blowouts). Methods have been published that apply methods of measuring or rating complexity, and interaction with other risks, and applying that to QRA models in a way that generates non-linear outcomes such as seen in some empirical research. |

|

Selected References: [23,24,25]

|

|

No RPs |

|

Discussion, Programs: As stated in TCM 7.1: Sometimes a project is part of a program or set of related projects. A program can be viewed as the top level on the WBS with the next level including the projects within the program. The basic project control concepts apply to a program with the added complication of integrating its projects. This same complication arises with contingency; each project manager in a program requires a contingency budget, and so to should the program director to address integrative risks that manifest themselves at the program level. This could be in addition to management reserve. As with control, the same QRA concepts apply to a program as for projects, but with different or compounded risks.

Discussion, Portfolios: Managing a portfolio of projects is usually part of an overall business asset or capital management process as opposed to program/project management per se. Portfolio risk analysis is more from a financial planning viewpoint of how much capital is needed and when considering changing business strategy and needs over time, and uncertain performance (i.e., risks) of programs and projects that make up the portfolio. Because portfolio management tracks projects over time, the data captured can be used to improve individual project QRA methods and models (e.g., if projects are over/under spending their contingency, calibrate the contingency method or p-value funded). |

|

Selected References: [26,27,28]

|

|

No RPs |

|

Discussion: The definition of management reserves (MR), and its distinction from contingency was discussed earlier. Given that MR determination is at management discretion, there are no specific RPs. However, there are generally two approaches to determination. The first is to address management’s general risk tolerance and is typically funded at some elevated probability of underrun value (e.g., p70 to 90) with MR being the difference between this value and contingency (usually set at p50 or the mean). The other approach is for funding low probability, high impact risks not amenable to contingency funding (e.g., funding a small value based on p x i is illogical). The Hollmann reference below suggests removing those risks from the contingency QRA and probabilistically analyzing each potential high impact/low probability (HILP), risk separately for decision making by the business. Both methods can be applied at management discretion. Management reserve can be established at a program level as well. |

|

|

No RPs |

|

Discussion: Discussion: Analytics is shorthand for QRA algorithms and methods developed using machine learning and artificial intelligence (ML/AI). These methods depend on having quality data. These methods will likely come to dominate the QRA world in the future. At this time, the parametric method covered in RP 42R-08, which is based on “manual” regression analysis of data, can be viewed as a baby-step toward machine learning based QRA algorithms and methods of the future. Eventually, AI applications will tie QRA ever closer to, or embedded in, decision making algorithms. The AACE “Data Science & Advanced Analytics” (DSAA) technical subcommittee and transactions should be followed because references in this field will quickly become dated. |

|

Selected References: [31]

|

8. Application of QRA in Strategic Asset (Portfolio) Management

|

TCM 3.2 – Asset Planning: This process is focused on identifying potential alternative solutions (including projects but also other options) to asset portfolio needs and requirements. The analysis of alternatives often takes place as a business planning process (i.e., asset portfolio management) outside the stage-gate process (see #1). Unclassified/Class 10 estimates for projects with >10 years, with associated QRA considerations (see section on Class 10) are often applied in early asset life cycle cost analyses in this process. Scenario or what-if analysis is often applied in this process (No RPs). |

|

TCM 3.3 - Investment Decision Making: In general, decision analysis of alternatives in consideration of risk as covered by TCM 3.3 is a separate topic with the exception of decision trees (RP 85R-14) which can also be employed in general QRA practice. Decision analysis involves more inputs than the capital cost and schedule risks covered by the QRA methods in this RP (e.g., must consider revenue and OPEX as well as CAPEX in NPV analysis). However, there are three areas where alignment between business decision analysis and project risk analysis is worth highlighting. One is that the start of the revenue stream in NPV analysis is directly driven by the project completion date quantified in project QRA. Another is that CAPEX price escalation and revenue (sell price) are driven by economic conditions and hence their analysis should be based on common assumptions and scenarios. Finally, the nature of a business’s interaction with stakeholders and project teams and the efficacy of its capital management system are systemic risks to a project; i.e., the business owns most project systemic risks to some extent. As was noted, the probabilistic escalation method generates a universal capex cost distribution that can be readily used in NPV models. |

|

9. Project Control Planning and Contingency Allocation

|

General Discussion:

The aggregation principle derives from the fact that risk quantification and contingency determination are stochastic and hence cannot be reliably allocated to lower level control accounts (e.g., activities, items or disciplines). While it is technically possible to drive project-specific risk impact quantification calculations to increasingly finite levels of cost or activity impact detail, this increasingly implies deterministic behavior. Quantifying systemic risk impacts is even more stochastic and less reliable. The authority principle means high-level WBS managers with wide authority may require contingency to deal with risks as they occur in the sub-project in their control. This justifies allocating contingency at an appropriate aggregation level. For this reason, the only RP for this topic is about contract risk allocation, not low-level cost account allocation which is generally not recommended.

For analysis by and allocation to sub-projects, QRA methods applicable to programs apply. |

|

|

|

Discussion:

|

10. Change Management and Contingency Management

|

|

|

No RPs |

|

TCM 10.3 - Change Management:

TCM 10.3.2.7 - Manage Contingency and Reserves: Stochastic Methods:

Deterministic Methods: |

|

Selected References: [33,34,35]

|

11. Maintain Methods and Tools Considering Historical Data

|

Discussion: The use of historical data is a principle of QRA methods per RP 40R-08. This is particularly true for parametric modeling (re: RP 42R-08) which is directly based on historical data using MLR. However, other methods rely on data to some extent. For example, history should inform the factors in predetermined guidelines, provide lessons learned and typical risk behavior for simulation analysis. Also, weather history is often used to inform quantification of weather event risks. It is also essential for the development of comparison metrics for validation methods. The capture and management of data to support QRA is the same process as for base estimating and schedule development purpose. An area of current and future practice development in respect to data analysis is machine learning and AI (ML/AI). While ML and AI may use unstructured data from many sources, in the near term, the focus of database development to support AI/ML for practical QRA applications is on structured data Follow the AACE Data Science & Advanced Analytics (DSAA) Technical Subcommittee and transactions where database development to support ML/AI is a key focus area. |

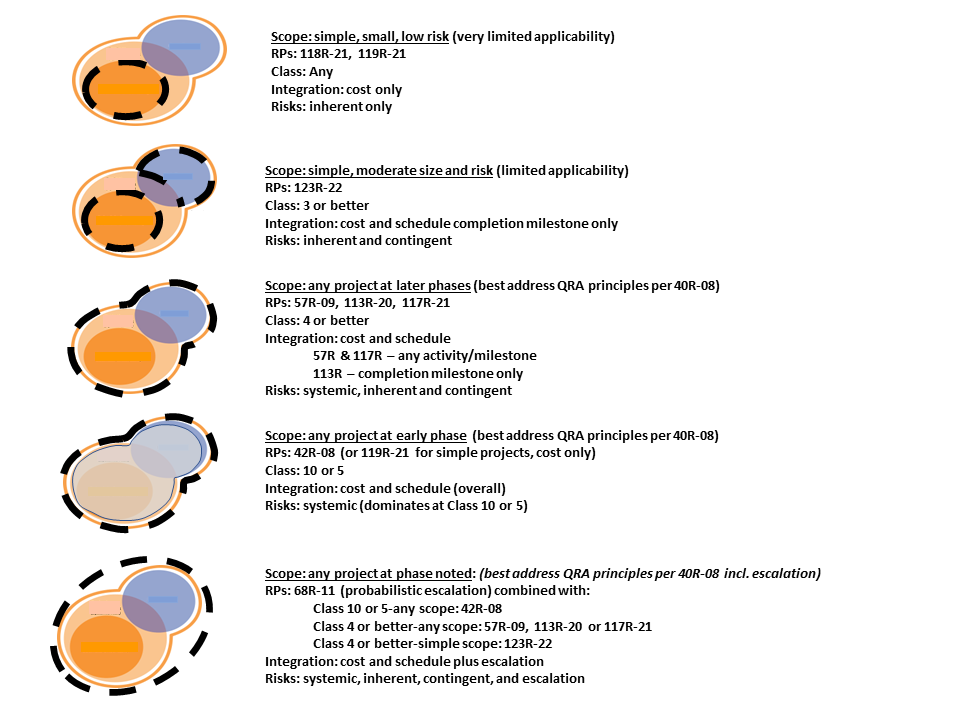

Figure 4 provides a guide to which QRA RP methods (listed in Section 7 and shown in the Figure 1 index map) are likely to be most fit-for-use in various project scope and risk situations (e.g., project complexity, estimate class, etc.). A Venn diagram is used to highlight applicability to various risk types (i.e., systemic, inherent and contingent) that are a key method selection determinant. The colors in the Venn diagram represent the following:

Blue: Contingent risks (i.e., risk events)

Dark Orange: Inherent risks (i.e., background variability)

Light Orange: Systemic risks (includes inherent and non-critical risk events)

The method selection factors summarized in Figure 4 include:

Risk type (re: Venn colors)

Scope (simple low-risk or more complex projects)

Estimate classification

Cost/schedule coverage/integration

The final selection always calls for reviewing and understanding the RPs themselves. Per the QRA maturity model (RP 122R-22), an organization at Level 3 or above maturity will have a suite of methods available to best meet its various needs.

Figure 4. QRA Method Application Guide

|

Hulett, David T., “Journey Map to a More Mature Schedule Risk Analysis (SRA) Process, Cost engineering Journal, AACE International, Morgantown, WV, March/April 2019. |

|

|

Hollmann, John, “Project Risk Quantification, Glossary”, Probabilistic

Publishing, Sugar Land TX, 2016. |

|

|

Hollmann, John, “Risk Analysis and Contingency Estimating for Class 10

Estimates”, AACE International Transactions, RISK-3908, AACE

International, Morgantown, WV, 2022. |

|

|

Dysert, Larry and T. Pickett, “Supporting Estimates with Effective Scope

of Work Definition”, 2020 AACE International Transactions, EST-3424,

AACE International, Morgantown, WV, 2020. |

|

|

Ahmad, Mir M. and Christopher Carson, “Capital Improvement Program

Stage-Gate Planning and Scheduling”, 2019 AACE International

Transactions, PS-3112, AACE International, Morgantown, WV, 2019. |

|

|

Carson, Christopher W. and Leo Carson-Penalosa, "Implementation of an Integrated Phase-Gate Project Controls Process", 2023 AACE International Transactions, TCM-4048, AACE International, Morgantown, WV, 2023 |

|

|

Barshop, Paul, “Capital Projects: What Every Executive Needs to Know to

Avoid Costly Mistakes and Make Major Investments Pay Off”, John Wiley &

Sons, Inc., Hoboken, New Jersey, 2016. |

|

|

Stephenson, L. and M. Pruneau, “Strategic Portfolio Management:

Improving Capital Utilization and Competitive Advantage”, 2016 AACE

International Transactions, TCM-2110, AACE International, Morgantown,

WV, 2016. |

|

|

Hollmann, J., (Presentation Only) “Cost Estimate Classification

Overview”, EST-3480, 2020 AACE International Virtual Conference & Expo. |

|

|

Zaheer, Syed H. and C. Fallows, “Document Project Readiness by Estimate

Class Using PDRI”, 2011 AACE International Transactions, EST-604, AACE

International, Morgantown WV, 2011. |

|

|

CII Project Definition Rating Index (PDRI) Overview. |

|

|

Opfer, Neil, “Where & Why Value Engineering Goes Wrong with Capital Projects”, 2021 AACE International Transactions, TCM-3707, AACE International, Morgantown WV, 2021. |

|

|

Dell’Isola, Michael D., “Better Use of Value Engineering in Project

Delivery”, Cost Engineering, Vol. 56, No. 06, AACE International,

Morgantown, WV, 2014. |

|

|

Lozon, Jim and G. Jergeas, “The Use and Impact of Value Improving

Practices and Best Practices”, Cost Engineering, Vol. 50, No. 06, AACE

International, Morgantown, WV, 2008. |

|

|

Zangeneh, Pouya, L. McMullan, M. Pearson, and B. McCabe, 2021 AACE

International Transactions, TCMA-3733, AACE International, Morgantown,

WV, 2021. |

|

|

Stephenson, H. Lance and P. Bredehoeft, “Benchmarking for Competitive

Advantage”, 2020 AACE International Transactions, TCMA-3502, AACE

International, Morgantown, WV, 2020. |

|

|

Devine, J. Michael and Rob Adkison, “Reference Class Forecasting: Theory

and Practical Application”, 2019 AACE International Transactions,

OWN-3056, AACE International, Morgantown, WV, 2019. |

|

|

Steiman, Samuel and Dr. David T. Hulett, “Identifying the Most Probable

Cost – Schedule Values from a Joint Confidence Level (JCL) Risk

Analysis”, AACE International Transactions, RISK-3111, AACE

International, Morgantown, WV, 2019. |

|

|

Hollmann, John K., “Realistic and Practical Project Risk Quantification

(Without CPM)”, Cost Engineering, Vol. 60, No. 04, AACE International,

Morgantown, WV, 2018. |

|

|

Wenger, Natalia and Jochun W. Lai, “Project Cost Management in Multiple

Currencies: A Case Study”, 2014 AACE International Transactions,

CSC.1711, AACE International, Morgantown, WV, 2014. |

|

|

Fritsche, Hans, “Transaction Exposure Management in International

Construction”, 1994 AACE International Transactions, INT.8, AACE

International, Morgantown, WV, 1994. |

|

|

Hollmann, John, “Project Risk Quantification", Chapter 13: Probabilistic

Escalation and Currency Exchange”, Probabilistic Publishing, Sugar Land

TX, 2016. |

|

|

Ogilvie, Alexander, “A Tale of Two Tails: Chaos in

Estimating Predictability”, Cost Engineering, Vol. 59, No. 03, AACE

International, Morgantown, WV, 2017. |

|

|

Raydugin, Yuri, “Non-Linear Probabilistic (Monte Carlo) Modeling of

Systemic Risks”, 2018 AACE International Transactions, RISK-2808, AACE

International, Morgantown, WV, 2018. |

|

|

Hollmann, John, “Risk Analysis at the Edge of Chaos”, Cost Engineering,

Vol. 57, No. 01, AACE International, Morgantown WV, 2015. |

|

|

Stephenson, H. Lance and Robert Gerber, “Strategic Portfolio Management:

Funding and Finance Methodologies”, 2020 AACE International

Transactions, TCM-3503, AACE International, Morgantown, WV, 2020. |

|

|

Alves, Ricardo Gonçalves, “Portfolio Management: Case Study of a

Brazilian Mining Company”, 2019 AACE International Transactions,

PM-3085, AACE International, Morgantown, WV 2019. |

|

|

Hollmann, John, “Project Risk Quantification", Chapter 7: Introduction

to Risk Quantification Methods, Probabilistic Publishing, Sugar Land TX,

2016. |

|

|

Vinueza, J. Gustavo, “Optimizing Your Management Reserve”, 2019 AACE

International Transactions, OWN-3236, AACE International, Morgantown,

WV, 2019. |

|

|

Hollmann, John, “Project Risk Quantification", Chapter 12: Project

Specific Risks and the Expected Value Method, Probabilistic Publishing,

Sugar Land TX, 2016. |

|

|

Hovhannisyan, Vahan, Peter Zachares, Alan Mosca, Yael Grushka-Cockayne, and Carlos Ledezma, "Data-Driven Schedule Risk Forecasting for Construction Mega-Projects", 2023 AACE International Transactions, DSAA-4101, AACE International, Morgantown, WV, 2023 |

|

|

Stephenson, H. Lance, “Strategic Portfolio Management: Asset Management

Model”, 2021 AACE International Transactions, TCM-3775, AACE

International, Morgantown, WV, 2021. |

|

|

Stephenson, H, Lance, “Change Management for the Project Life Cycle”,

2022 AACE International Transactions, TCM-3934, AACE International,

Morgantown WV, 2022 |

|

|

Hollmann, John, “Project Risk Quantification", Chapter 17: Budgeting for

Risks and Account Control , Probabilistic Publishing, Sugar Land TX,

2016. |

|

|

Stroemich, Christopher, and M. Dissanayake, “Project Risk Drawdown – A

Structured Approach to Contingency Management”, 2018 AACE International

Transactions, RISK-2795, AACE International, Morgantown, WV, 2018. |

Disclaimer: The content provided by the contributors to this professional guidance document is their own and does not necessarily reflect that of their employers, unless otherwise stated.

March 18, 2024 Revision:

John K. Hollmann, PE CCP CEP DRMP FAACE Hon. Life (Primary Contributor)

Editorial, added links to recent RPs and several reference papers

August 23, 2022 Revision:

John K. Hollmann, PE CCP CEP DRMP FAACE Hon. Life (Primary Contributor)

Editorial, added links to 117R-21

January 31, 2022 Revision:

John K. Hollmann, PE CCP CEP DRMP FAACE Hon. Life (Primary Contributor)

December 20, 2019 Revision:

John K. Hollmann, PE CCP CEP DRMP

FAACE Hon. Life (Primary Contributor)

Dr. Manjula Dissanayake, CCP

This document is copyrighted by AACE International and may not be reproduced without permission.